Overview

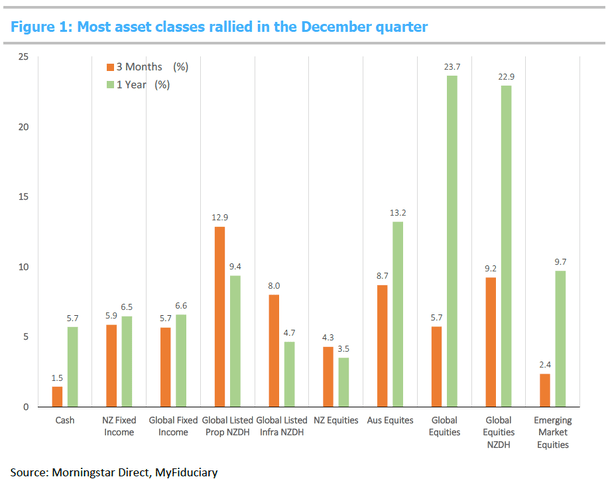

Most asset classes performed well over the December quarter…

…as markets became more convinced that a global soft -landing scenario is the most likely outcome for the years ahead.

Gains were strongest in US equities over the past year, in part reflecting the relative strength of the US economy.

Interest rates were slashed to historic lows in 2008/9 and remained at exceptionally low levels until late 2021.

Central banks believed until recently that the balance of inflation vs. deflationary risks favoured keeping rates low. It took CPI inflation surging past 5% to shift this view.

Inflated asset prices are a direct consequence of having rates so low for so long.

The increase in rates since 2022 has re-set asset prices, with the notable exception of residential property which may take a long time to adjust to more ‘rational’ levels.

Click on the link below to read the full report.