- Taking the NZ Income Scheme to all Kiwi’s

David Boyle

Mint Asset Management

In 1986 I bought a Fiat 124 Sport 1800 coupe. As I signed the ownership papers, my dad’s words were ringing in my ears about how unreliable they were and how costly they were to run. But I knew better and my mind was made up.

It was the coolest car I had ever had. Not that I had much of a benchmark to go by. My first car was a Morris Minor 850cc (well actually it was Dad’s) split windscreen 55 and then, to keep up with my mates, I bought a 1979 SR Toyota Corolla. When I drove my 124 Sport for the first time I thought I had made it. The throaty rumble through the exhaust, quick acceleration, and flash cassette deck, required little guessing who was driving down the road by the locals and, unfortunately, the local traffic officers as well.

Those were the days when there were no Japanese imports, cars were very expensive, and European cars more so because, while they looked cool, they were pretty unreliable, parts were hard to come by and they spent just as much time in the garage getting fixed as they did on the road. Of course, that wasn’t going to happen to me.

I had just accepted a job in Christchurch and, one month before I was set to head up to the big smoke, the unthinkable happened. The car blew a head gasket and a piston at the same time. I had no idea what that meant but I knew it was not good. In fact, it was terrible. It would cost me $4,000 to fix the motor, which was just under half of what I had paid for the car earlier that year.

I needed the car, I couldn’t sell the car as it was, so it had to be fixed. What saved my bacon was that I had built up an emergency savings account and, while it didn’t cover the total cost, I had some long-term savings for my first house which I was able to dip into. I hated touching my savings, but to get a personal loan unsecured was going to cost 18% and I was only earning around $7,500 a year, so it made sense to use my savings. If I hadn’t had that money I would have been in a world of trouble.

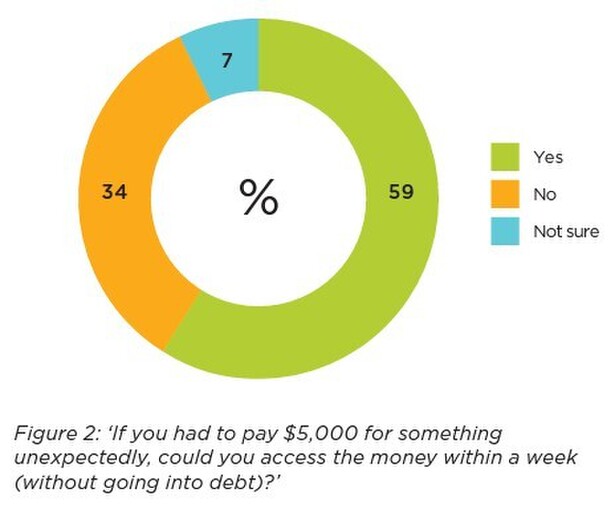

In a recently released survey by the Financial Services Council called ‘Financial Resilience Trends in New Zealand’, a number of topics have been researched for a couple of years now. They look at New Zealanders’ financial confidence, financial wellbeing, financial literacy, but the one that worried me the most (and has for quite a long time) was the financial preparedness of Kiwis. Just under 30% of those surveyed had less than one month’s buffer. In other words, if they lost their job they could not meet their financial outgoings. Another 35% had less than six months’ buffer. This does not take into account any of life’s bumps like illness, accidents or, in my case, car breakdowns.

It’s no surprise then that 58% of those surveyed were either not prepared or not particularly prepared for their retirement years. I mean, if you don’t have enough in the short-term to cover life’s emergencies then the chance of feeling good about your retirement would be like living on planet La La right?

Which leads me to the most recent government initiative that is looking to create a new scheme, much like ACC is today but in this case is for workers who are made redundant or can’t work for a period of time. Essentially, a New Zealand Income Insurance scheme that all employers and employees will contribute to. With over 100,000 Kiwis being made redundant each year, with many getting no or little financial support from their employers, on the face of it it seems like a good idea.

The key features of the proposed New Zealand Income Insurance Scheme are:

- Broad coverage for different working arrangements

- Coverage for job losses due to redundancy, layoffs and health conditions and disabilities

- A four-week notice period and four-week payment, at 80% of salary, from employers

- A further six months of financial support from the scheme, at 80% of wages or a salary

- Option to extend support for up to 12 months for training and rehabilitation

- A case management service to support people’s return to work

- Administered by ACC

- Funded by levies on wages and salaries, with both workers and employers paying an estimated 1.39% each

- Workers would become eligible after six months of levy contributions in the previous 18 months

Now I am not saying this is a good or bad approach and there is a lot of water to go under the bridge before it happens. But it does lead me back to my old hobby horse, which offers an alternative solution: building a universal approach to help Kiwis save and build an emergency fund or what’s starting to be referred as a “Side Car” savings account for those unexpected life events.

The above scheme is catering for around 3.8% of New Zealanders each year who lose their job for a range of reasons. My simplistic view is that, instead of building a big pot for only those who might need it in time, why not allow individuals the chance to build the buffer themselves. It’s like that old proverb “Give a man a fish you feed him for a day, teach a man to fish and you feed him for a lifetime”.

Given that the employer and the employee are both required to make to contributions, why not have those funds in their own name for their own specific emergencies?

The new proposal says contribution rates will be around 1.4% each for the employer and employee. So, looking at an example where an individual earning $61,000, the median wage in NZ as at June 2022, this means the annual contribution would be $1,708 to the new scheme. The thing is, only around 3.55% of the population will likely draw or need the money at any given year if they were made redundant.

This is what got me thinking. Another option is for that money to go into your own individual emergency fund. While this won’t help anyone who is made redundant in the short term, it will over time help Kiwis build that buffer, but also improve their savings habit, and have funds available for them to help them manage any of life’s curve balls.

In the short term there will be more cost to the government (but that is mainly there now) with social support and benefits being funded from taxes. However, looking over generations to come, the buffer will not only improve New Zealanders’ resilience to life’s shocks, but their overall wellbeing as well, because the worry of the emergency of the day has been removed. More importantly it will reduce government expenditure over time because there will be reduced dependency for other social services that are currently being provided today.

As that saving habit grows and reaches a limit that is appropriate for any short-term emergency, those future contributions could then be allocated to their KiwiSaver account. If an event did occur - health issue, redundancy etc - the contributions would be reallocated to their sidecar savings until the savings account was back up to its pre-determined level.

Even better, there would be very little additional set-up costs given we (unlike most other OECD countries in the world) have a central contributions collection process, via the Inland Revenue, that we use for KiwiSaver. The funds would simply be allocated to an account or fund that could be added to the central collection scheme, via the employer, which would have some clear rules around access so it would be easy to administer by the account provider.

Another benefit, in time, would be to alleviate the current hardship withdrawal process we have to access KiwiSaver funds. The cost of delivery and time to get funds is incredibly challenging, not only for the providers but also the stress it causes those needing the funds. Notwithstanding the impact those withdrawals would have on their long-term retirement savings.

I thought you might be interested to know that I did get the car fixed. I took it up to Christchurch and, a few months later, decided to sell the car to help replace my savings, and trade down back to the Morris Minor. I will never forget the day when Dad gave me not only the keys to the car but a wry old smile, saying what he didn’t have to say out loud and that was: I told you so.

Disclaimer: David Boyle is Head of Sales and Marketing at Mint Asset Management Limited. The above article is intended to provide information and does not purport to give investment advice.

Mint Asset Management is the issuer of the Mint Asset Management Funds. Download a copy of the product disclosure statement here.